Muscat VAT Corporate Tax Strategy for SME Owners Navigating Oman’s New Tax Reality

Understanding Muscat VAT Corporate Tax Strategy Fundamentals

Why the distinction matters for operational stability

Muscat VAT Corporate Tax Strategy is now one of the most important financial disciplines for business owners operating in Oman, yet it remains one of the most misunderstood. Many SME founders in Muscat still treat VAT and Corporate Tax as similar reporting obligations when in reality they serve completely different economic functions. VAT is a transactional tax collected on behalf of the government at each stage of commercial exchange, while Corporate Tax is a direct levy on the profits a company earns over a financial year. This confusion often leads to incorrect pricing models, distorted profit expectations, and weak cash management. When business owners fail to design their Muscat VAT Corporate Tax Strategy properly, the result is not only compliance risk but also structural inefficiency that quietly erodes profitability. Oman’s regulatory environment has matured rapidly, and authorities now expect businesses to demonstrate both technical compliance and strategic awareness. SMEs that continue to blur VAT and Corporate Tax roles frequently miscalculate margins, underfund future liabilities, and struggle when audits or reviews arise. Understanding how these taxes interact within the same business ecosystem is the foundation of sustainable financial leadership in today’s Omani market.

Operational Consequences of Poor Muscat VAT Corporate Tax Strategy

How cash flow pressure is created by misunderstanding tax mechanics

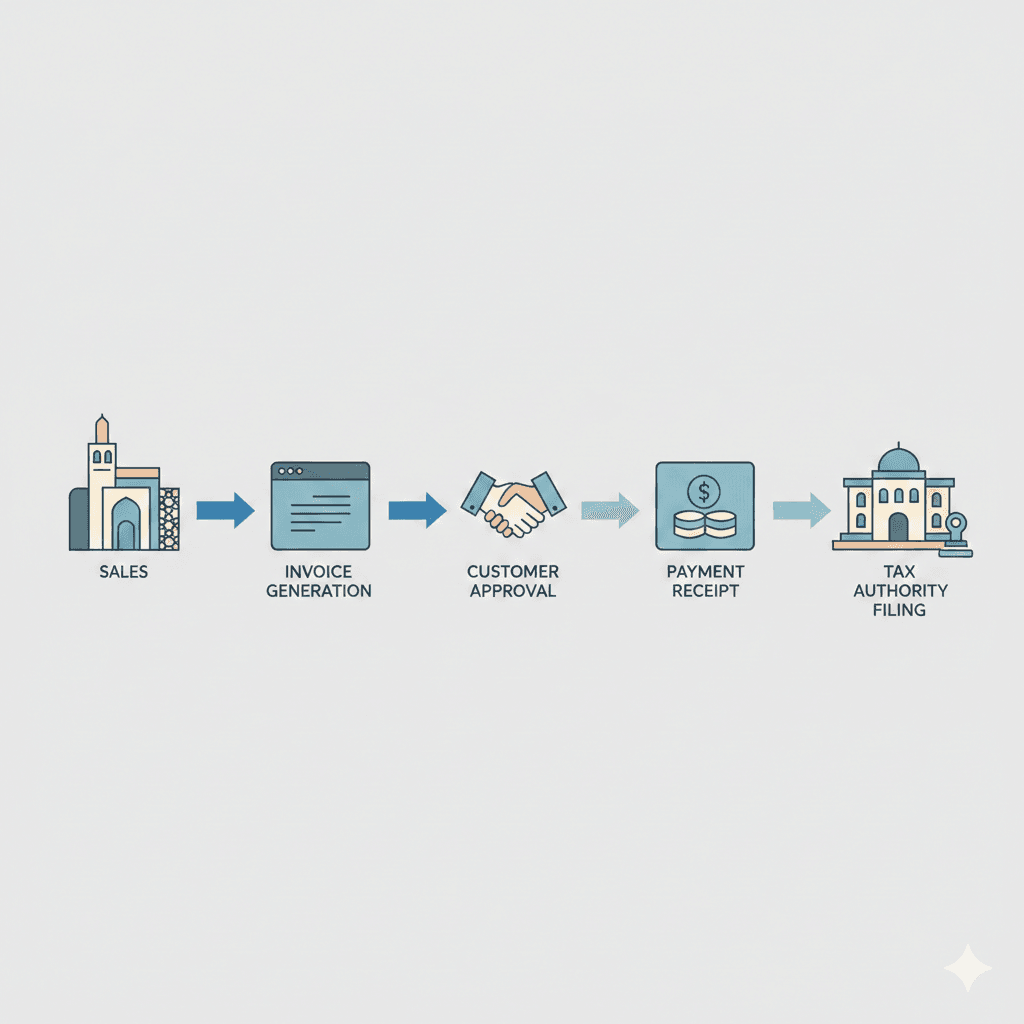

A flawed Muscat VAT Corporate Tax Strategy quickly translates into daily operational stress. VAT affects cash flow in real time, as businesses collect tax from customers and remit it to the Tax Authority on scheduled cycles. Corporate Tax, on the other hand, materializes after profits are calculated at year end. Many Muscat entrepreneurs mistakenly treat VAT collections as available working capital, which artificially inflates liquidity until the VAT return becomes due. When payment deadlines arrive, companies suddenly face cash shortages that disrupt supplier payments, payroll, and growth plans. This mismanagement is one of the most common reasons profitable SMEs in Oman still experience chronic cash pressure. A disciplined Muscat VAT Corporate Tax Strategy separates operational funds from tax obligations at the accounting level and within management reporting. When owners can clearly see what belongs to the business and what belongs to the government, decision-making improves dramatically. Leaderly regularly observes that businesses implementing this distinction early experience smoother expansion and lower financial volatility across the year.

Building a Compliant Muscat VAT Corporate Tax Strategy from Day One

Aligning structure, reporting, and leadership behavior

Developing an effective Muscat VAT Corporate Tax Strategy begins long before returns are filed. It starts with the legal and accounting structure chosen at incorporation, the pricing model used in sales contracts, and the internal controls governing invoicing and expense recognition. VAT requires precise documentation and strict adherence to invoicing rules, while Corporate Tax relies on accurate profit measurement supported by compliant financial statements. SMEs that integrate these requirements into their operational design from the outset avoid expensive retroactive corrections. A strong Muscat VAT Corporate Tax Strategy also demands leadership discipline. Owners who personally understand the mechanics of VAT and Corporate Tax are better equipped to evaluate financial performance, approve investments, and assess growth opportunities with confidence. Advisory support becomes most powerful when it is embedded into strategy, not added later as damage control.

Why Muscat VAT Corporate Tax Strategy Shapes Growth Planning

Tax positioning as a competitive advantage

Growth decisions in Oman are increasingly influenced by the quality of a company’s Muscat VAT Corporate Tax Strategy. Expansion into new product lines, cross-border transactions, or larger contracts all carry specific VAT and Corporate Tax implications that directly affect net profitability. Many Muscat business owners underestimate how much strategic planning can improve outcomes simply by optimizing tax positioning within legal boundaries. A well-designed Muscat VAT Corporate Tax Strategy allows SMEs to forecast tax exposure accurately, structure deals more efficiently, and avoid unnecessary leakage of earnings. This level of planning transforms taxation from a reactive burden into a proactive business tool. Financial advisors working closely with leadership teams help translate regulatory complexity into practical models that guide sustainable scaling in Oman’s competitive market.

Risk Management Through Muscat VAT Corporate Tax Strategy Discipline

Preventing regulatory exposure before it appears

Risk in taxation rarely announces itself loudly. It accumulates quietly through inconsistent records, misunderstood exemptions, and informal practices that were once tolerated but are no longer acceptable under Oman’s evolving enforcement standards. A disciplined Muscat VAT Corporate Tax Strategy establishes systematic review processes, reconciliations, and internal audits that detect weaknesses before they escalate. This approach protects SMEs not only from penalties but also from reputational harm that can affect financing, partnerships, and customer confidence. When leaders view tax management as part of enterprise risk management rather than administrative compliance, the entire organization becomes more resilient. Leaderly’s advisory experience shows that companies adopting this mindset navigate regulatory change with far greater confidence and stability.

Leadership Responsibility in Muscat VAT Corporate Tax Strategy Execution

From technical compliance to executive ownership

Ultimately, Muscat VAT Corporate Tax Strategy is a leadership responsibility, not merely an accounting task. While finance teams and external advisors execute the technical work, ownership must remain with directors and founders. When leadership understands the strategic consequences of VAT and Corporate Tax decisions, they can align investment, financing, and operational priorities accordingly. This clarity strengthens governance, improves lender relationships, and enhances long-term valuation. In Oman’s SME environment, where many businesses remain founder-led, this executive ownership of tax strategy is often the decisive factor separating stable enterprises from those perpetually reacting to financial surprises.

The most successful SMEs in Muscat are those that internalize Muscat VAT Corporate Tax Strategy as part of their core management philosophy rather than a regulatory afterthought. By recognizing the distinct roles of VAT and Corporate Tax and integrating them into everyday financial decision-making, owners gain control over cash flow, improve forecasting accuracy, and reduce systemic risk. This disciplined approach creates transparency across the organization, enabling teams to operate with confidence even as Oman’s tax environment continues to mature.

For business owners seeking long-term sustainability, Muscat VAT Corporate Tax Strategy is not about minimizing tax alone; it is about building financial architecture that supports growth, protects value, and withstands regulatory scrutiny. When SMEs align sound accounting practices with thoughtful advisory insight and proactive leadership, taxation becomes a stabilizing force rather than a disruptive one. This perspective empowers Omani entrepreneurs to navigate complexity with clarity and to build enterprises that thrive in both opportunity and accountability.

#Leaderly #MuscatVATCorporateTaxStrategy #Oman #Muscat #SMEs #Accounting #Tax #Audit