Muscat Internal Audit Plan as a Practical Annual Control Program

Muscat Internal Audit Plan as a Management Tool, Not a Compliance Burden

A Muscat Internal Audit Plan is often misunderstood by SME owners as a formal document prepared only when regulators, banks, or investors ask questions. In reality, it should operate as a living management framework that helps business leaders understand how money, authority, and risk move through the organisation. For SMEs in Oman, this distinction matters because most operational failures do not come from fraud or intentional misconduct, but from undocumented processes, unclear responsibilities, and assumptions that no one has formally tested. An effective plan shifts internal review away from box-ticking and toward decision support. It helps founders see whether cash handling matches contracts, whether approvals reflect real authority, and whether reporting timelines support management decisions. When designed properly, the plan fits the scale of the business rather than copying large corporate models that overwhelm small teams. It should also reflect the Omani operating environment, where VAT compliance, supplier documentation, and labour-related controls interact closely with daily operations. By positioning the Muscat Internal Audit Plan as a practical annual program rather than a one-off exercise, SMEs gain a structured way to review their business before problems become expensive disputes or regulatory issues.

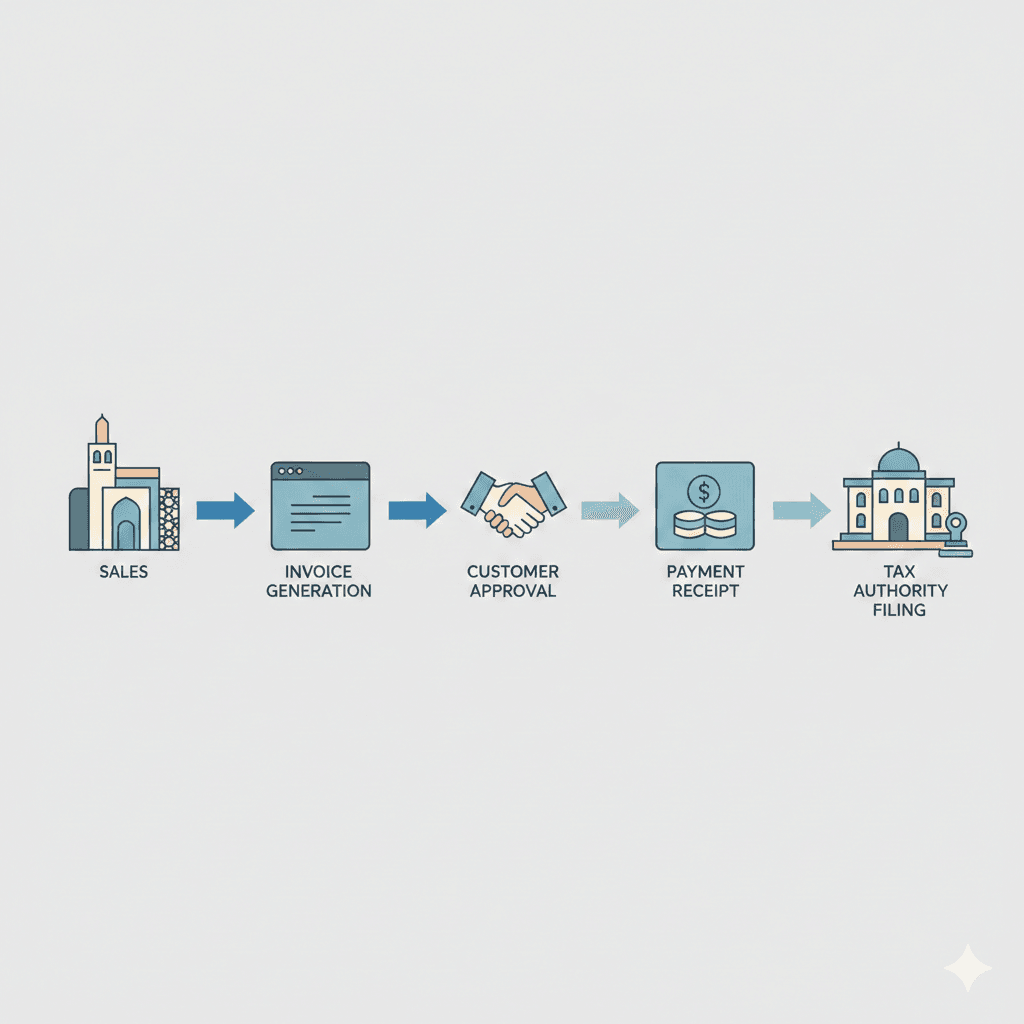

Muscat Internal Audit Plan Scope Built Around Real SME Risk Areas

The strength of a Muscat Internal Audit Plan depends less on its length and more on how intelligently its scope is defined. For SMEs in Muscat, the highest-risk areas are usually predictable: revenue recognition, expense approvals, payroll accuracy, VAT treatment, and contract management. A focused plan does not attempt to review everything at once. Instead, it prioritises processes where errors would directly affect cash flow, tax exposure, or owner liability. This approach respects the limited time and resources of SME teams while still delivering meaningful insight. Each area included in the plan should have a clear objective, such as verifying whether invoices align with signed agreements or whether expense claims follow documented approval limits. Importantly, scope decisions should be reviewed annually, as business models evolve quickly in Oman’s growing SME ecosystem. A company expanding into new services, locations, or financing arrangements introduces new risks that must be reflected in the plan. When scope is grounded in actual operations, the internal review becomes relevant to management discussions, not an abstract exercise detached from day-to-day realities.

Muscat Internal Audit Plan Documentation That Supports Decision-Making

Documentation is where many SMEs struggle, not because records do not exist, but because they are scattered, inconsistent, or poorly explained. A Muscat Internal Audit Plan should define what evidence is required, where it is stored, and how it supports conclusions. This does not mean creating excessive paperwork. It means ensuring that key documents such as contracts, reconciliations, VAT workings, and approval trails can be traced and understood by someone other than the person who prepared them. For owner-managed businesses, this discipline is particularly important, as knowledge often sits in one individual’s head. Clear documentation protects continuity and reduces dependence on informal explanations. It also strengthens discussions with external advisors, auditors, and tax specialists by providing a coherent narrative of how controls operate. In practice, SMEs that invest modest effort into organising their internal review files find that year-end reporting, tax filings, and financing conversations become smoother. Documentation within the plan should be practical, proportionate, and designed to answer management questions, not to impress external reviewers.

Muscat Internal Audit Plan Scheduling Across the Financial Year

Timing is a critical but overlooked element of an effective Muscat Internal Audit Plan. Many SMEs attempt to review everything at year-end, when teams are already under pressure from reporting deadlines and operational demands. A more effective approach spreads internal reviews across the financial year, aligning them with business cycles. For example, revenue testing may be more meaningful after peak sales periods, while payroll and expense reviews can follow annual salary adjustments or bonus payments. This staggered scheduling reduces disruption and allows management to act on findings while the year is still in progress. It also reinforces the idea that internal review is part of normal operations, not an emergency response. In Oman, where VAT reporting and compliance obligations follow defined cycles, aligning review activities with filing timelines adds further value. Issues identified early can be corrected before they result in penalties or reputational damage. A well-paced plan supports continuous improvement rather than retrospective damage control.

Muscat Internal Audit Plan Roles and Independence in SME Structures

One of the most sensitive aspects of a Muscat Internal Audit Plan for SMEs is deciding who performs the review. In smaller organisations, complete independence is rarely possible, but objectivity can still be achieved through thoughtful role allocation. The plan should clearly state who reviews each area and how conflicts of interest are managed. For example, a finance manager may prepare reconciliations but should not be the sole reviewer of their accuracy. In owner-led businesses, founders often need external perspective to challenge long-standing assumptions. This is where periodic involvement of experienced advisors adds value, not by replacing internal knowledge, but by testing it. Clear role definition builds credibility in the findings and ensures that issues are addressed constructively rather than defensively. When responsibilities are documented within the plan, discussions about control weaknesses become professional and solution-focused, supporting healthier governance as the business grows.

Muscat Internal Audit Plan Outcomes That Feed Advisory Decisions

The ultimate purpose of a Muscat Internal Audit Plan is not to produce reports, but to inform better decisions. Findings should translate into practical actions, whether updating approval limits, refining VAT processes, or reconsidering contract structures. For SMEs in Oman, internal review outcomes often intersect with broader advisory needs such as business valuation, feasibility assessments, or preparation for financing and restructuring. When internal insights are captured clearly, they provide a reliable foundation for these strategic discussions. This is where alignment with experienced advisory support becomes natural rather than forced. A plan that highlights control gaps or process inefficiencies creates a roadmap for targeted improvement, rather than vague recommendations. Over time, SMEs that treat internal review outcomes as inputs into management strategy develop stronger resilience and credibility in the market.

For SMEs operating in Oman, a Muscat Internal Audit Plan represents a shift from reactive compliance to proactive control. When designed around real risks, scheduled intelligently, and documented clearly, it becomes a practical annual program that supports daily management rather than interrupting it. The value lies not in formality, but in clarity: understanding how the business actually operates and where it is exposed.

By embedding this discipline into the business cycle, SME owners and finance managers gain confidence in their numbers, their controls, and their decisions. This clarity supports smoother tax compliance, more effective external assurance, and stronger advisory conversations, allowing businesses to grow with structure rather than uncertainty.

#Leaderly #MuscatInternalAuditPlan #Oman #Muscat #SMEs #Accounting #Tax #Audit